Chapter 9 Two-sample tests

9.1 Motivation

Question: Is there some form of dependence between two variables \(X\) and \(Y\)? Does the knowledge about the realization of \(X\) also convey information about \(Y\)?

Often: One of the variables (\(Y\)) is the dependent variable, the other (\(X\)) is independent or explanatory. If both variables enter equally, the roles may also be interchangeable.

Exploratory: Bivariate exploratory analysis (see Chapter 4.2).

Inference: Various tests for the hypothesis pair

- \(H_0:\) Independence of \(X\) and \(Y\).

- \(H_1:\) Some form of dependence between \(X\) and \(Y\).

Testing procedures differ depending on the scale level of the two variables but also with respect to the type of putative form of dependence under the alternative.

| Dep. vs. expl. | Quantitative | Qualitative |

|---|---|---|

| Quantitative | Correlation tests (Pearson, Spearman, …) |

2- and k-sample tests (t-test, analysis of variance, Wilcoxon-Mann-Whitney, …) |

| Qualitative | Logistic regression (bi-, multinomial, …) |

\(\chi^2\)-test, Fisher’s exact test, … |

Initially: Consider the 2-sample problem, i.e., a dependent quantitative variable \(Y\) and a binary explanatory variable \(X\). The binary variable \(X\) splits the variable \(Y\) into two subsamples.

Jargon: 2-sample testing is also known as A/B testing, especially for randomized experiments with two experimental conditions.

Especially: Popular jargon in e-commerce. Under varying setups of a web page, assess:

- Revenue generated.

- Click-through rate.

- Number of purchases.

- Transactions per user.

9.2 Comparison of distributions

Task: Assess several distributions for differences.

- \(H_0:\) All samples come from the same distribution.

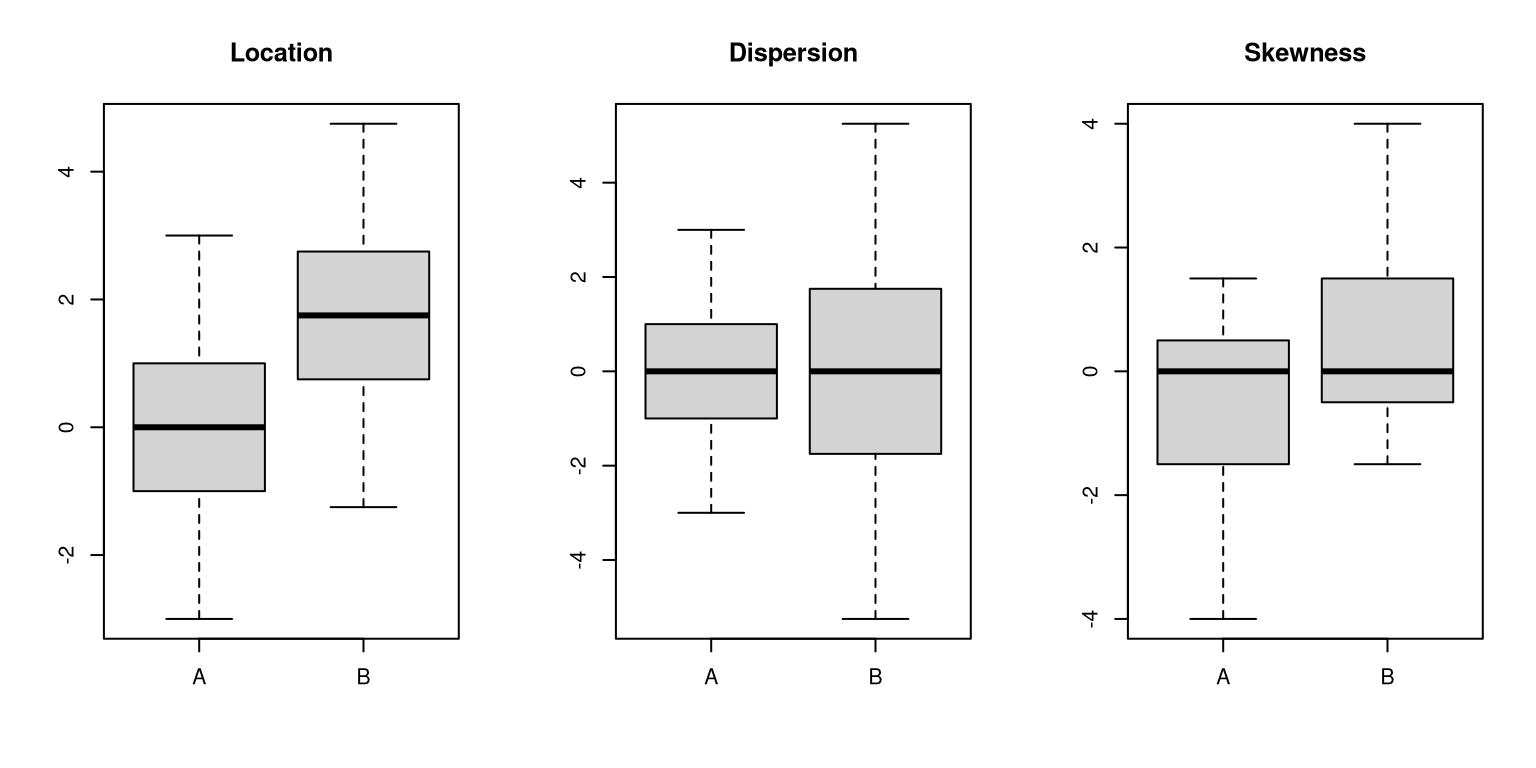

- \(H_1:\) At least one sample comes from another distributions (i.e., differs in some way such as location, dispersion, or skewness).

Idea: Although the distributions often differ in more than one of these properties, it is in principle possible that only one of location, dispersion, or skewness differs while the other properties are the same (see below). While location differences are of most interest in many applications, also dispersion differences may be of interest (e.g., when comparing different techniques to measure measurement techniques for a certain element in a chemical compound) or skewness differences (e.g., when assessing the risk in different financial products).

Initially: Compare two samples for location differences.

Data: Myopic loss aversion (MLA) experiment.

## invest gender male age treatment grade arrangement

## 1 70.0000 female/male yes 11.7533 long 6-8 team

## 2 28.3333 female/male yes 12.0866 long 6-8 team

## 3 50.0000 female/male yes 11.7950 long 6-8 team

## 4 50.0000 male yes 13.7566 long 6-8 team

## 5 24.3333 female/male yes 11.2950 long 6-8 team

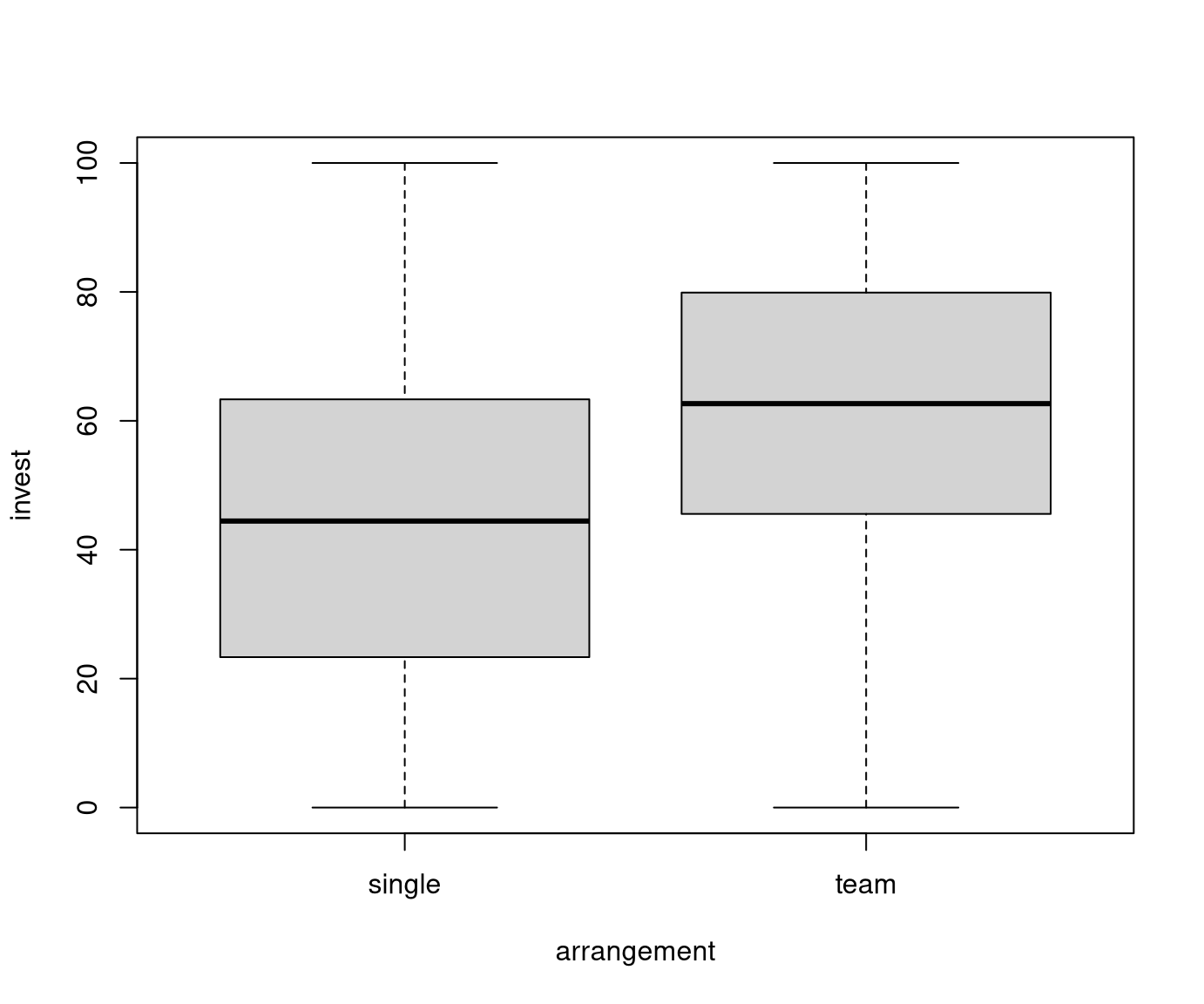

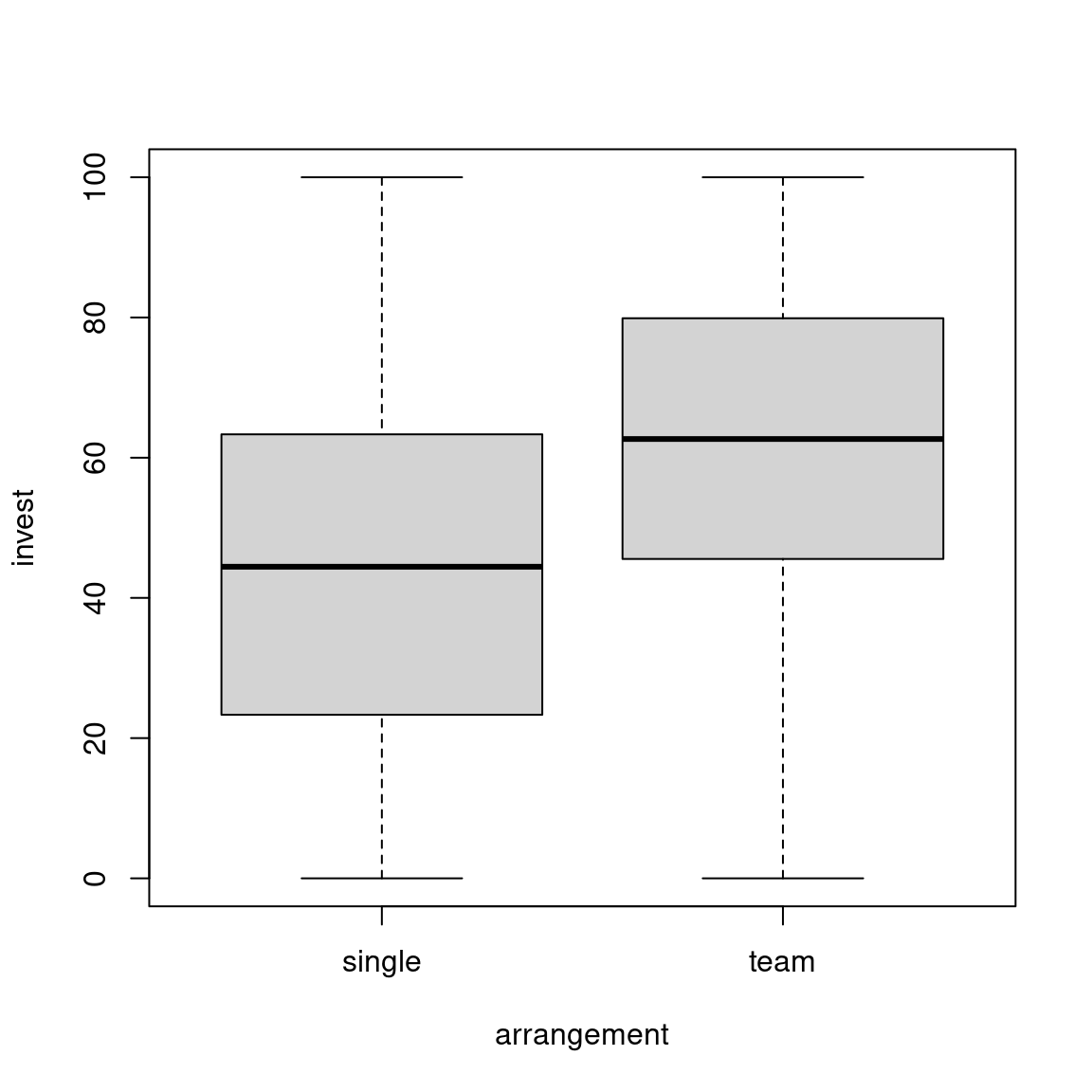

## 6 83.0000 male yes 11.8366 long 6-8 teamHere: Consider dependence of the main outcome variable invest on the experimental factor arrangement (single vs. team).

Group-wise statistics:

| Single | Team | Overall | |

|---|---|---|---|

| \(n\) | 385 | 185 | 570 |

| \(\overline y\) | 45.0 | 61.5 | 50.4 |

| \(Q_{0.5}\) | 44.4 | 62.7 | 50.0 |

| \(s\) | 26.2 | 24.5 | 26.8 |

| \(\mathit{IQR}\) | 40.0 | 34.3 | 40.0 |

| Min | 0 | 0 | 0 |

| Max | 100 | 100 | 100 |

9.3 Location differences

Intuitive: To assess whether invest depends on the explanatory variable arrangement, the empirical mean investment in the two arrangements can be compared: \(45.0\) (single) and \(61.5\) (team).

Simple idea: To test for significant location differences, the differences of the means (\(45.0 - 61.5 = -16.5\)) can be used and standardized by a suitable standard error.

Formally: Consider two independent random variables \(Y_A\) and \(Y_B\). The corresponding expectations are \(\text{E}(Y_A) = \mu_A\) and \(\text{E}(Y_B) = \mu_B\), respectively.

Question: Are the expectations \(\mu_A\) and \(\mu_B\) the same?

Answer: Test

\[\begin{array}{lrcl} H_0: & \mu_A & = & \mu_B \\ H_1: & \mu_A & \neq & \mu_B \end{array}\]based on empirical data.

Remark: Initially we assume that the two variable may only differ in location, i.e., other moments of the distributions are the same. In particular, the variances are equal \(\text{V}(Y_A) = \text{V}(Y_B) = \sigma^2\).

Notation:

- \(n_A\) observations from \(Y_A\) with realizations \(y_{A,1}, \dots, y_{A,n_A}\).

Corresponding empirical mean \(\overline y_A\) and variance \(s_A^2\). - \(n_B\) observations from \(Y_B\) with realizations \(y_{B,1}, \dots, y_{B,n_B}\).

Corresponding empirical mean \(\overline y_B\) and variance \(s_B^2\).

Intuitive: Consider difference of empirical means \(\overline y_A - \overline y_B\).

Question: How large is the random variation of this difference?

Answer:

\[\begin{eqnarray*} \text{E}(\overline Y_A - \overline Y_B) & = & \mu_A - \mu_B \\ \text{V}(\overline Y_A - \overline Y_B) & = & \frac{\text{V}(Y_A)}{n_A} + \frac{\text{V}(Y_B)}{n_B} \; = \; \frac{n_A + n_B}{n_A \cdot n_B} \cdot \sigma^2 \end{eqnarray*}\]

9.4 Two-sample \(t\)-test

Test statistic: Scaled difference of the means

\[ t \quad = \quad \frac{\overline y_A - \overline y_B}{\widehat{\mathit{SD}}}. \]

Scaling: Estimate the standard deviation \(\sigma^2\) of the observations and plug it into the standard deviation for the difference of the means.

\[ \widehat{\mathit{SD}} \quad = \quad \sqrt{ \frac{n_A + n_B}{n_A \cdot n_B} \cdot \frac{(n_A - 1) \cdot s_A^2 + (n_B - 1) \cdot s_B^2}{n_A + n_B - 2} }. \]

Null distribution: Under \(H_0\) and assuming both \(Y_A\) and \(Y_B\) are normally distributed, this \(t\)-statistic is \(t\)-distributed with \(n-2\) degrees of freedom. For increasing \(n-2\) the \(t\)-distribution converges to a standard normal distribution.

Central limit theorem (CLT): For any distribution of \(Y_A\) and \(Y_B\) the statistic \(t\) is asymptotically standard normal under \(H_0\).

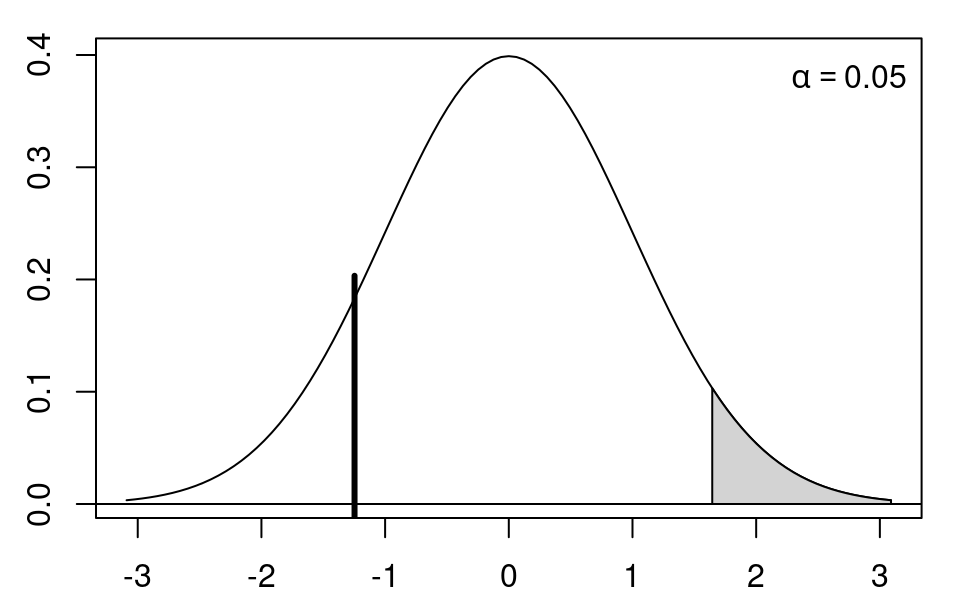

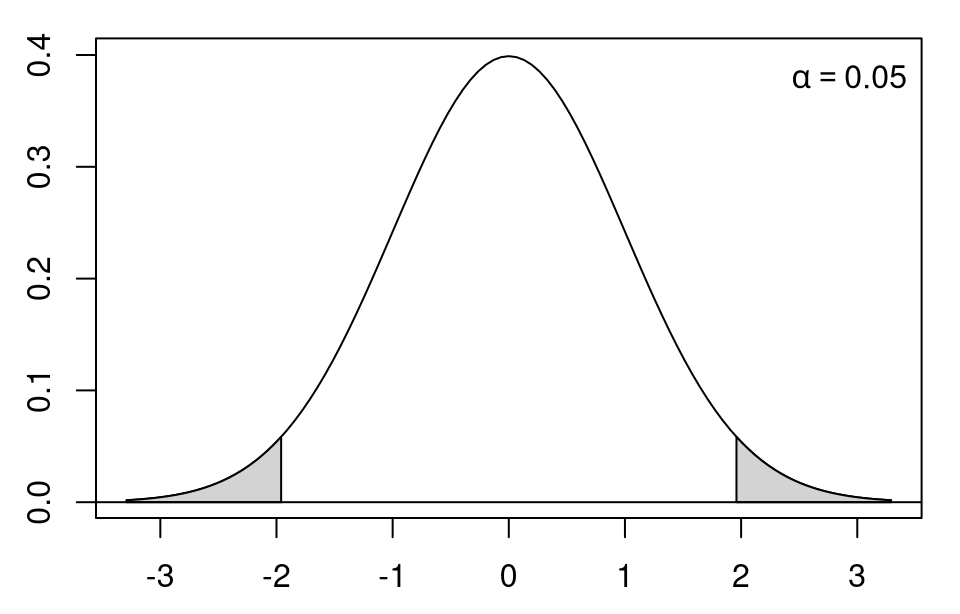

Critical values: The 2-sided critical values at significance level \(\alpha\) are \(\pm t_{n-2; 1 - \alpha/2}\), i.e., \(\pm\) the \((1 - \alpha/2)\) quantile of the \(t_{n-2}\) distribution. Rule of thumb: The critical values at the \(\alpha = 0.05\) level are approximately \(t_{n-2; 0.975} \approx 2\).

Test decision: Reject the null hypothesis if \(|t| > t_{n-2; 1 - \alpha/2}\).

\(p\)-value: Analogously compute the corresponding \(p\)-value \(p = P_{H_0}(|T| > |t|)\). Reject the null hypothesis if \(p < \alpha\).

Confidence interval: The level \(\alpha\) confidence interval for the true difference in expectations \(\Delta = \mu_A - \mu_B\) can also be computed based on the critical values.

\[\begin{equation*} \left[ \hat \Delta ~-~ t_{n-2; 1 - \alpha/2} \cdot \widehat{\mathit{SD}} ~;~~ \hat \Delta ~+~ t_{n-2; 1 - \alpha/2} \cdot \widehat{\mathit{SD}} \right] \end{equation*}\]

Example: Assume that the difference of empirical means is \(\hat \Delta = 3\) and the estimated standard deviation is \(\widehat{\mathit{SD}} = 2\). Then \(t = 3/2 = 1.5\). Thus, the null hypothesis cannot be rejected at 5% level.

Illustration: Differences of mean investment between single players and teams.

| Single | Team | |

|---|---|---|

| \(n\) | 385 | 185 |

| \(\overline y\) | 45.0 | 61.5 |

| \(s\) | 26.2 | 24.5 |

Test: Assess equality of mean investments at 5% significance level.

Test statistic:

\[\begin{eqnarray*} \widehat{\mathit{SD}} & = & \sqrt{ \frac{385 + 185}{385 \cdot 185} \cdot \frac{(385 - 1) \cdot 26.2^2 + (185 - 1) \cdot 24.5^2}{385 + 185 - 2} } \\ & = & 2.30 \\ t & = & \frac{45.0 - 61.5}{ 2.30} \\ & = & -7.19. \end{eqnarray*}\]

Thus, this is much smaller than \(t_{568; 0.025} = -1.96\).

Interpretation: Single players invest significantly less than teams.

In R:

##

## Two Sample t-test

##

## data: invest by arrangement

## t = -7.194, df = 568, p-value = 1.99e-12

## alternative hypothesis: true difference in means between group single and group team is not equal to 0

## 95 percent confidence interval:

## -21.0466 -12.0193

## sample estimates:

## mean in group single mean in group team

## 45.0124 61.5453

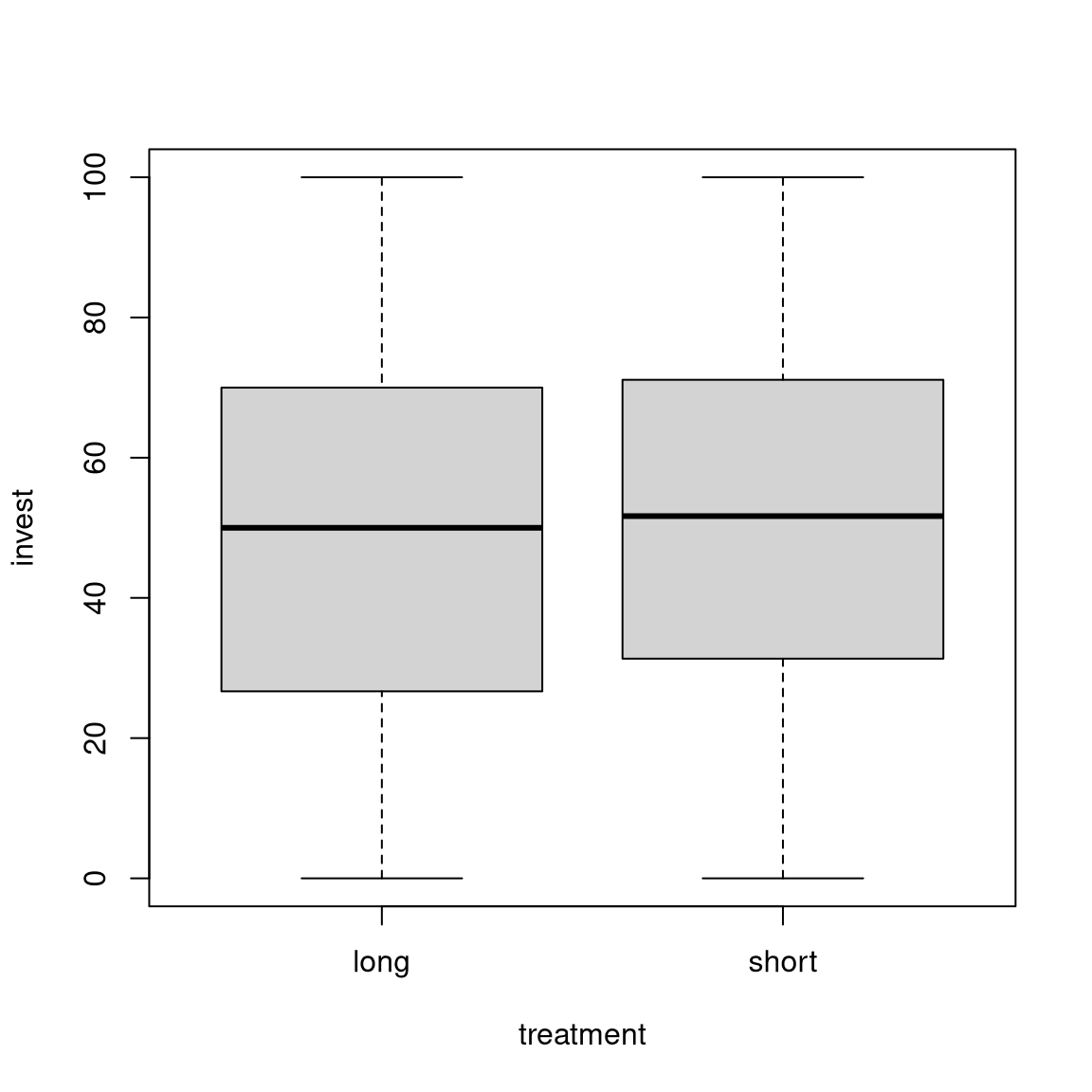

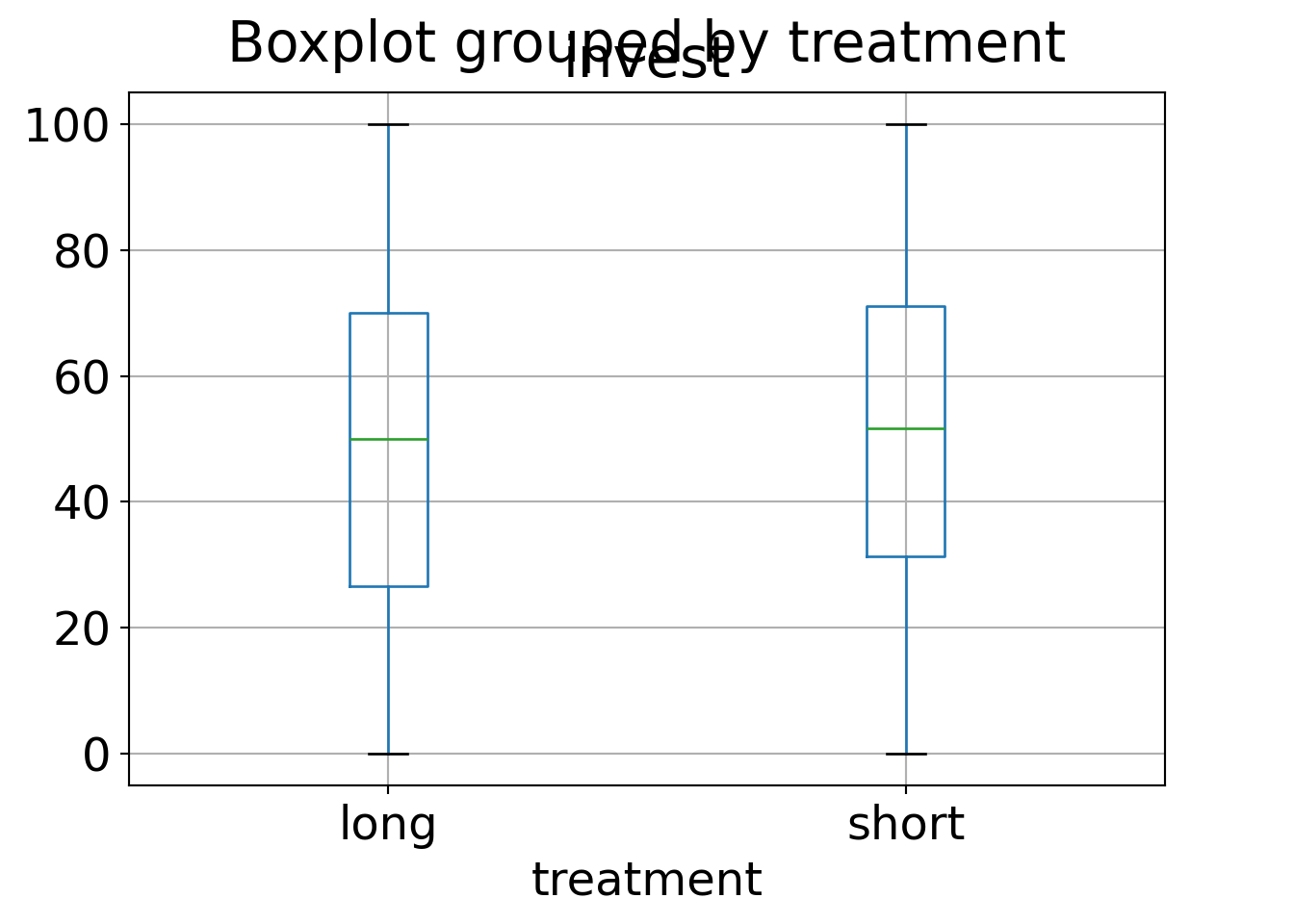

Illustration: Differences of mean investment between long and short treatment.

| Long | Short | |

|---|---|---|

| \(n\) | 285 | 285 |

| \(\overline y\) | 49.0 | 51.8 |

| \(s\) | 26.7 | 26.9 |

Test: Can we show at 5% significance level that investments are lower in the short treatment than in the long treatment?

Test statistic:

\[\begin{eqnarray*} \widehat{\mathit{SD}} & = & \sqrt{ \frac{285 + 285}{285 \cdot 285} \cdot \frac{284 \cdot 26.7^2 + 284 \cdot 26.9^2}{568} } \\ & = & 2.25 \\ t & = & \frac{49.0 - 51.8}{ 2.25} \\ & = & -1.25. \end{eqnarray*}\]

Thus, this is not greater than \(t_{568; 0.05} = -1.65\).

Interpretation: Investments in the short treatment are not significantly lower.

In R:

##

## Two Sample t-test

##

## data: invest by treatment

## t = -1.269, df = 568, p-value = 0.897

## alternative hypothesis: true difference in means between group long and group short is greater than 0

## 95 percent confidence interval:

## -6.54609 Inf

## sample estimates:

## mean in group long mean in group short

## 48.9544 51.8023Question: How to estimate the standard deviation when the variances \(\text{V}(Y_A) \neq \text{V}(Y_B)\)?

Answer: Compute the \(t\)-statistic with

\[ \widehat{\mathit{SD}} \quad = \quad \sqrt{ \frac{s_A^2}{n_A} + \frac{s_B^2}{n_B} }. \]

Null distribution: Under \(H_0\) the resulting \(t\)-statistic is approximately \(t_\delta\)-distribution with degrees of freedom

\[ \delta \quad = \quad \frac{% \left( \frac{s_A^2}{n_A} + \frac{s_B^2}{n_B} \right)^2 }{% \frac{s_A^4}{n_A^2 (n_A - 1)} + \frac{s_B^4}{n_B^2 (n_B - 1)} }. \]

Name: Welch \(t\)-test.

In R:

##

## Welch Two Sample t-test

##

## data: invest by arrangement

## t = -7.371, df = 386.6, p-value = 1.04e-12

## alternative hypothesis: true difference in means between group single and group team is not equal to 0

## 95 percent confidence interval:

## -20.9431 -12.1228

## sample estimates:

## mean in group single mean in group team

## 45.0124 61.5453##

## Welch Two Sample t-test

##

## data: invest by treatment

## t = -1.269, df = 567.9, p-value = 0.897

## alternative hypothesis: true difference in means between group long and group short is greater than 0

## 95 percent confidence interval:

## -6.5461 Inf

## sample estimates:

## mean in group long mean in group short

## 48.9544 51.80239.5 Tutorial

For illustrating various 2-sample questions, data from an economic experiment

on myopic loss aversion MLA is used (Glätzle-Rützler, Sutter, Zeileis 2015.

No Myopic Loss Aversion in Adolescents? - An Experimental Note,

Journal of Economic Behavior & Organization, 111, 169-176).

The pupils participating in this experiment could invest in a lottery with

positive expectation over nine rounds. The risk-neutral choice would be to

always invest 100% of the points possible. However, due to risk aversion

or loss aversion many subjects typically invest less. The main research

question in this experiment, however, is whether this loss aversion effect

is enhanced when investments are made by short-term rather than long-term

decisions (myopia). The data set can be downloaded as MLA.csv or MLA.rda.

9.5.1 Setup

R

## invest gender male age treatment grade arrangement

## 1 70.0000 female/male yes 11.7533 long 6-8 team

## 2 28.3333 female/male yes 12.0866 long 6-8 team

## 3 50.0000 female/male yes 11.7950 long 6-8 teamPython

# Make sure that the required libraries are installed.

# Import the necessary libraries and classes:

import pandas as pd

import numpy as np

from matplotlib import pyplot as plt

import seaborn as sns

pd.set_option("display.precision", 4) # Set display precision to 4 digits in pandas and numpy.# Load dataset

MLA = pd.read_csv("MLA.csv", index_col=False, header=0)

# Preview the first 5 lines of the loaded data

MLA.head()## invest gender male age treatment grade arrangement

## 0 70.0000 female/male yes 11.7533 long 6-8 team

## 1 28.3333 female/male yes 12.0866 long 6-8 team

## 2 50.0000 female/male yes 11.7950 long 6-8 team

## 3 50.0000 male yes 13.7566 long 6-8 team

## 4 24.3333 female/male yes 11.2950 long 6-8 team9.5.2 2 samples: Exploratory analysis

The dependent variable is invest, the average invested points across all 9 rounds.

The main treatment is whether the players could change investment decisions

in every round (short) or only for three rounds in a row (long).

Another important factor that was varied in the experiment is the

arrangement, i.e., whether investments were made by single players or

by teams of two. Both of these experimental factors will be used in the

following to create a 2-sample setup.

Further explanatory variables that will be used later on are the

gender of the (team of) player(s), an indicator whether

(at least one of) the player(s) (in the team) was male, the (average)

age, and the school grade (6-8 vs. 10-12).

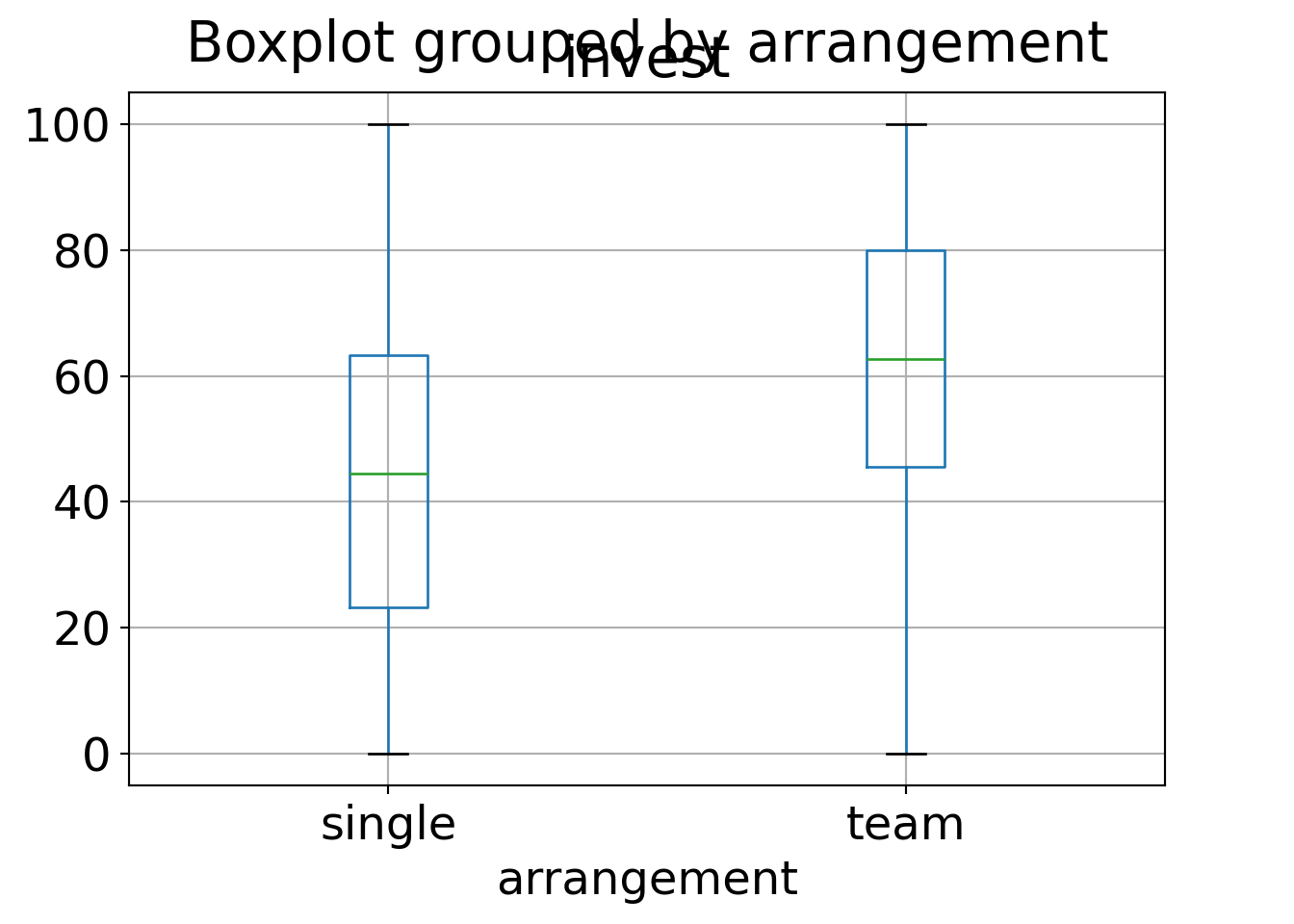

An exploratory visualization using parallel boxplots shows that the arrangement

appears to have an clear effect on invest (with teams behaving more rational

than single players) while the main treatment seems to have no effect at all

(i.e., the pupils do not seem to be affected by myopia).

We obtain the corresponding 2-sample statistics (first only means in both arrangement groups):

Obtain all summary statistics shown in the lecture slides:

R

In R, we could employ repeated tapply() calls. Or, alternatively, we could put together a small

function that computes all the summary statistics in one vector:

mystats <- function(x) c(n = length(x), mean = mean(x),

median = median(x), sd = sd(x), iqr = IQR(x), min = min(x), max = max(x))This can then be applied to both single and team players as well as to the entire sample:

tab <- tapply(MLA$invest, MLA$arrangement, mystats)

cbind(

Single = tab$single,

Team = tab$team,

All = mystats(MLA$invest)

)## Single Team All

## n 385.0000 185.0000 570.0000

## mean 45.0124 61.5453 50.3784

## median 44.4444 62.6667 50.0000

## sd 26.2414 24.4932 26.8094

## iqr 40.0000 34.3333 40.0000

## min 0.0000 0.0000 0.0000

## max 100.0000 100.0000 100.0000Python

We obtain many of the summary statistics from the describe() function.

## count mean std min 25% 50% 75% max

## arrangement

## single 385.0 45.0124 26.2414 0.0 23.3333 44.4444 63.3333 100.0

## team 185.0 61.5453 24.4932 0.0 45.5556 62.6667 79.8889 100.0To obtain all summary statistics shown in the lecture slides, we could employ the aggregation agg() function.

from scipy.stats import iqr

# Compute summary statistics for each group (single and team)

tab = MLA.groupby("arrangement")["invest"].agg(n=len,

mean=np.mean,

median=np.median,

sd=np.std,

iqr=iqr,

min=min,

max=max)## <string>:3: FutureWarning: The provided callable <function mean at 0x7f43797c8d60> is currently using SeriesGroupBy.mean. In a future version of pandas, the provided callable will be used directly. To keep current behavior pass the string "mean" instead.

## <string>:3: FutureWarning: The provided callable <function median at 0x7f4365efc400> is currently using SeriesGroupBy.median. In a future version of pandas, the provided callable will be used directly. To keep current behavior pass the string "median" instead.

## <string>:3: FutureWarning: The provided callable <function std at 0x7f43797c8ea0> is currently using SeriesGroupBy.std. In a future version of pandas, the provided callable will be used directly. To keep current behavior pass the string "std" instead.

## <string>:3: FutureWarning: The provided callable <built-in function min> is currently using SeriesGroupBy.min. In a future version of pandas, the provided callable will be used directly. To keep current behavior pass the string "min" instead.

## <string>:3: FutureWarning: The provided callable <built-in function max> is currently using SeriesGroupBy.max. In a future version of pandas, the provided callable will be used directly. To keep current behavior pass the string "max" instead.## n mean median sd iqr min max

## arrangement

## single 385 45.0124 44.4444 26.2414 40.0000 0.0 100.0

## team 185 61.5453 62.6667 24.4932 34.3333 0.0 100.0Analogously, we could obtain 2-sample statistics for invest grouped by treatment.

9.5.3 2-sample \(t\)-test

The classical parametric test for assessing the null hypothesis of equal distributions against location differences is the 2-sample \(t\)-test. Assuming both subsamples come from normal distributions with the same variance reduces null hypothesis and alternative to: \(\mu_A = \mu_B\) vs. \(\mu_A \neq \mu_B\).

R

This \(t\)-test can be carried out with t.test() and options var.equal = TRUE. Applying this to the MLA data

shows that there is a highly-significant difference between single players and teams

regarding the level of investments (or degree of loss aversion):

##

## Two Sample t-test

##

## data: invest by arrangement

## t = -7.194, df = 568, p-value = 1.99e-12

## alternative hypothesis: true difference in means between group single and group team is not equal to 0

## 95 percent confidence interval:

## -21.0466 -12.0193

## sample estimates:

## mean in group single mean in group team

## 45.0124 61.5453Python

Perform a 2-sample \(t\)-test.

from statsmodels.stats.weightstats import ttest_ind

single = MLA[MLA['arrangement']=="single"]['invest']

team = MLA[MLA['arrangement']=="team"]['invest']

ttest = ttest_ind(x1=single, x2=team, alternative="two-sided", usevar="pooled")

print("t = {:.1f}, p-value = {:.1g}, df = {:.0f}".format(ttest[0],ttest[1],ttest[2]))## t = -7.2, p-value = 2e-12, df = 568In addition to the two-sided alternative \(\mu_A \neq \mu_B\) it is possible to

also assess the one-sided alternatives \(\mu_A > \mu_B\) (alternative = "greater")

and \(\mu_A < \mu_B\) (alternative = "less").

This is useful for assessing the main treatment effect in the MLA data. Economic

theory would suggest that mean investments should be greater in the long

condition compared to the short condition. The corresponding \(t\)-test can be

conducted with:

R

##

## Two Sample t-test

##

## data: invest by treatment

## t = -1.269, df = 568, p-value = 0.897

## alternative hypothesis: true difference in means between group long and group short is greater than 0

## 95 percent confidence interval:

## -6.54609 Inf

## sample estimates:

## mean in group long mean in group short

## 48.9544 51.8023Python

long = MLA[MLA['treatment']=="long"]['invest']

short = MLA[MLA['treatment']=="short"]['invest']

ttest = ttest_ind(x1=long, x2=short, alternative="larger", usevar="pooled")

print("t = {:.1f}, p-value = {:.1g}, df = {:.0f}".format(ttest[0],ttest[1],ttest[2]))## t = -1.3, p-value = 0.9, df = 568This shows clearly that this cannot be significant for this data because the empirical average investment in the long condition is already lower than in the short condition.

Finally, the assumption of equal variances can be given up:

R

By using var.equal = FALSE which is the default in t.test().

##

## Welch Two Sample t-test

##

## data: invest by arrangement

## t = -7.371, df = 386.6, p-value = 1.04e-12

## alternative hypothesis: true difference in means between group single and group team is not equal to 0

## 95 percent confidence interval:

## -20.9431 -12.1228

## sample estimates:

## mean in group single mean in group team

## 45.0124 61.5453##

## Welch Two Sample t-test

##

## data: invest by treatment

## t = -1.269, df = 567.9, p-value = 0.897

## alternative hypothesis: true difference in means between group long and group short is greater than 0

## 95 percent confidence interval:

## -6.5461 Inf

## sample estimates:

## mean in group long mean in group short

## 48.9544 51.8023Python

By using usevar=unequal (usevar=pooled is the default).

ttest = ttest_ind(x1=single, x2=team, alternative="two-sided", usevar="unequal")

print("t = {:.1f}, p-value = {:.1g}, df = {:.0f}".format(ttest[0],ttest[1],ttest[2]))## t = -7.4, p-value = 1e-12, df = 387ttest = ttest_ind(x1=long, x2=short, alternative="larger", usevar="unequal")

print("t = {:.1f}, p-value = {:.1g}, df = {:.0f}".format(ttest[0],ttest[1],ttest[2]))## t = -1.3, p-value = 0.9, df = 568Note that then the \(t\)-distribution only holds approximately under the null hypothesis, even if the 2 samples come from normal distributions. This is known as the Welch approximation and the corresponding test as Welch 2-sample \(t\)-test.

For the MLA data setting var.equal = FALSE or TRUE in R or usevar=unequal or pooled in Python does not make much difference because variances across both arrangement and treatment are rather homogeneous anyway.