Chapter 8 Limited Dependent Variables

8.1 Introduction

Limited response variables: Mixed discrete and continuous features of the dependent variable.

Typical sources: Censoring and truncation.

Economic explanations:

- Corner solutions: Utility-maximizing choice of individuals is at the corner of the budget set, typically zero.

- Sample selection: Data deficiency causes response to be unknown (or different) for subsample.

- Treatment effects: Response for each individual is only observable for one level of a “treatment” variable.

Examples: Typical economic examples for limited responses.

- Labor supply.

\(y_i\): Number of hours worked by person \(i\).

Potential covariates: Education, non-work income, … - Expenditures for health services.

\(y_i\): Expenditures of person \(i\) for health services last month.

Potential covariates: Health status, income, gender, … - Wage equations.

\(y_i\): Earnings of person \(i\) derived from tax returns.

Potential covariates: Education, previous experience, … - Unemployment programs.

\(y_i\): Wage of person \(i\) after unemployment.

Treatment: Training program (potentially non-random assignment).

Potential covariates: Occupation, duration of unemployment, …

8.1.1 Example: PSID 1976 (Mroz data)

Cross-section data from the 1976 Panel Study of Income Dynamics (PSID), based on data for the previous year, 1975.

A data frame containing 753 observations on 21 variables, including:

| Variable | Description |

|---|---|

participation |

Did the individual participate in the labor force in 1975? (equivalent to wage \(> 0\) or hours \(> 0\)) |

hours |

Wife’s hours of work in 1975. |

youngkids |

Number of children less than 6 years old. |

oldkids |

Number of children between ages 6 and 18. |

age |

Wife’s age in years. |

education |

Wife’s education in years. |

wage |

Wife’s average hourly wage in 1975 (USD). |

fincome |

Family income in 1975 (USD). |

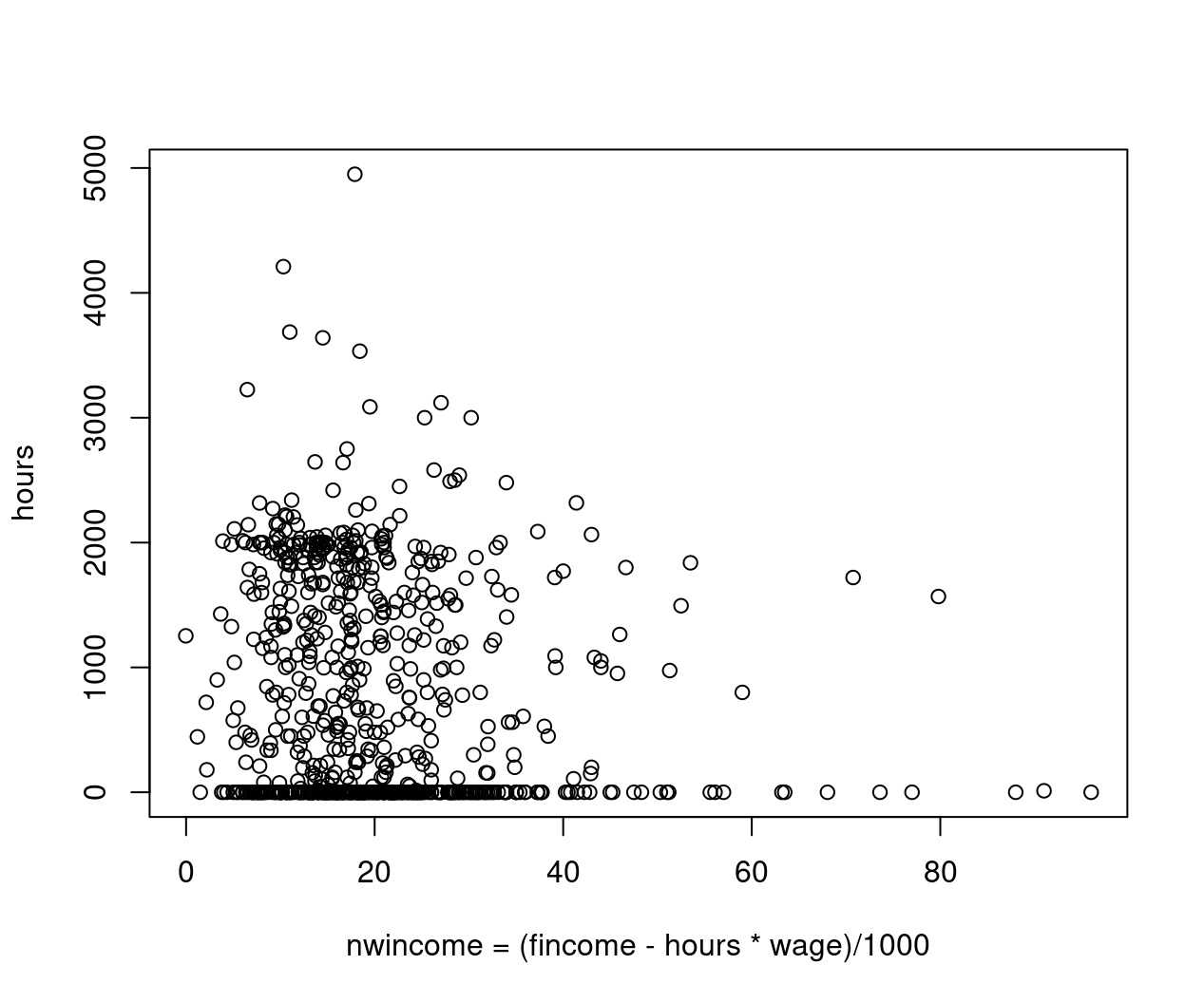

Example: Corner solution

Figure 8.1: Nonwife income against hours worked - jittered

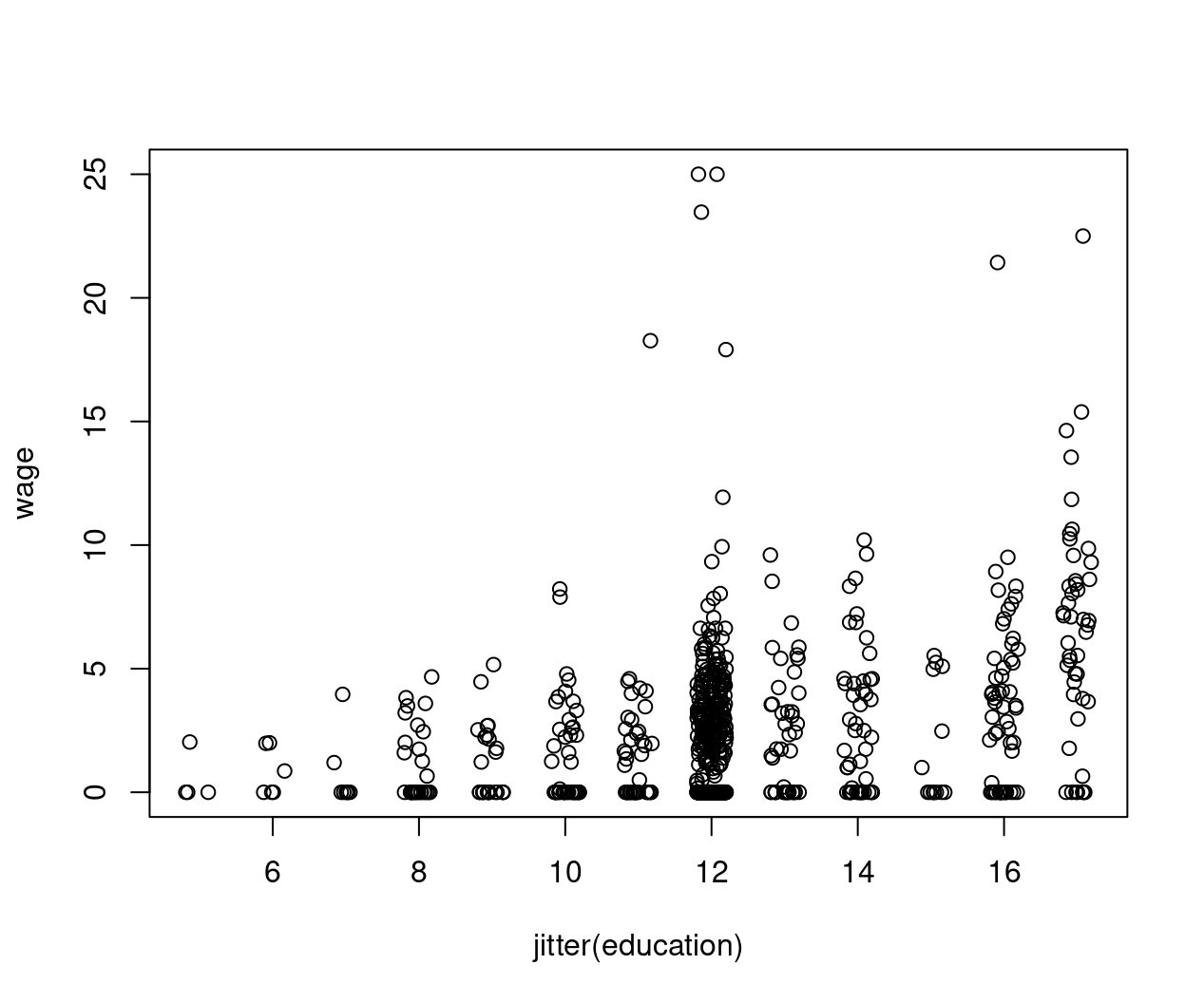

Example: Sample selection

Figure 8.2: Education against wage - jittered

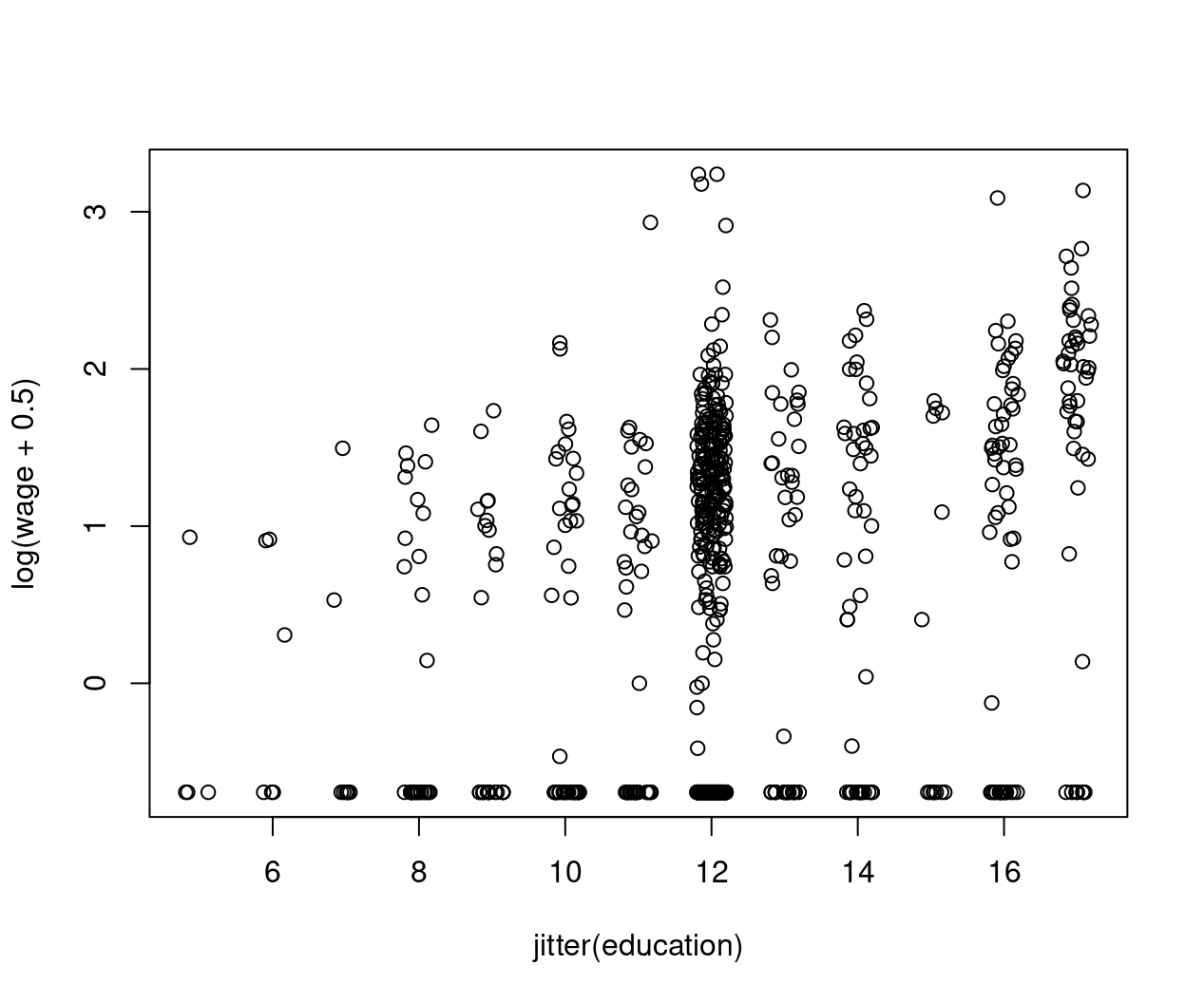

Figure 8.3: Education against log(wage+0.5) - jittered

8.2 Tobin’s Corner Solution Model

Problem: As motivated above, many microeconomic variables have

- non-negative values,

- a cluster of observations at zero.

Note: OLS cannot be used sensibly due to

- possibly negative predictions,

- imposed constant marginal effects (which cannot be remedied by logs as \(\log(0)\) is not defined).

Quantities of interest:

- \(\text{P}(y = 0 ~|~ x) = 1 - \text{P}(y > 0 ~|~ x)\), probability of zero.

- \(\text{E}(y ~|~ y > 0,~ x)\) expectation conditional on positive \(y\).

- \(\text{E}(y ~|~ x) = P(y > 0 ~|~ x) \cdot \text{E}(y ~|~ y > 0,~ x)\) expectation.

Ideas:

- Two-part model with binary selection and truncated outcome.

- Latent variable driving both selection and outcome.

Tobin’s solution: Employ the latter approach with latent Gaussian variable \(y^*\) and observed discrete-continuous response \(y\):

\[\begin{eqnarray*} y^* & = & x^\top \beta ~+~ \varepsilon, \qquad \varepsilon ~|~ x \sim \mathcal{N}(0, \sigma^2),\\ y\phantom{^*} & = & \max(0, y^*), \end{eqnarray*}\]

i.e., \(y\) is a censored version of \(y^*\).

Likelihood:

\[\begin{equation*} L(\beta, \sigma; y, x) ~=~ \prod_{i = 1}^n f(y_i ~|~ x_i, \beta, \sigma)^{I(y_i > 0)} \cdot \text{P}(y_i = 0 ~|~ x_i)^{I(y_i = 0)} \end{equation*}\]

where

\[\begin{eqnarray*} \text{P}(y_i = 0 ~|~ x_i) & = & \text{P}(y_i^* \le 0 ~|~ x_i) \\ & = & \Phi \left(\frac{0 - x_i^\top \beta}{\sigma} \right) ~=~ 1 - \Phi \left(\frac{x_i^\top \beta}{\sigma} \right) \\ f(y_i ~|~ x_i, \beta, \sigma) & = & \frac{1}{\sigma} \cdot \phi \left( \frac{y_i - x_i^\top \beta}{\sigma} \right) \end{eqnarray*}\]

Remarks:

- Model is known as tobit model.

- Despite the name it does not belong to the same model class as the binary logit and probit models.

- Log-likelihood can be shown to be globally concave.

- MLE is well-behaved (asymptotically normal etc.).

In R: tobit() from package AER. Convenience interface to survreg() from package survival which provides much more general regression tools for censored responses.

Alternatively: crch(..., left = 0) from package crch for censored regression with conditional heteroscedasticity. Dedicated interface for tobit-type models with either censoring or truncation, different response distributions (beyond normal).

Example: Regression for annual hours of work in PSID 1976 data, using reduced-form specification. Wage is missing as a regressor (as unobserved for non-working subsample).

Model equation of interest:

Fitting tobit model and naive OLS models:

hours_tobit <- tobit(hours_f, data = PSID1976)

hours_ols1 <- lm(hours_f, data = PSID1976)

hours_ols2 <- lm(hours_f, data = PSID1976,

subset = participation == "yes")Compare coefficients:

modelsummary(list("Tobit" = hours_tobit,

"OLS (all)" = hours_ols1,

"OLS (positive)" = hours_ols2),

fmt=3, estimate="{estimate}{stars}")| Tobit | OLS (all) | OLS (positive) | |

|---|---|---|---|

| (Intercept) | 965.305* | 1330.482*** | 2056.643*** |

| (446.436) | (270.785) | (346.484) | |

| nwincome | -8.814* | -3.447 | 0.444 |

| (4.459) | (2.544) | (3.613) | |

| education | 80.646*** | 28.761* | -22.788 |

| (21.583) | (12.955) | (16.434) | |

| experience | 131.564*** | 65.673*** | 47.005** |

| (17.279) | (9.963) | (14.556) | |

| I(experience^2) | -1.864*** | -0.700* | -0.514 |

| (0.538) | (0.325) | (0.437) | |

| age | -54.405*** | -30.512*** | -19.664*** |

| (7.419) | (4.364) | (5.894) | |

| youngkids | -894.022*** | -442.090*** | -305.721** |

| (111.878) | (58.847) | (96.450) | |

| oldkids | -16.218 | -32.779 | -72.367* |

| (38.641) | (23.176) | (30.361) | |

| Num.Obs. | 753 | 753 | 428 |

| R2 | 0.266 | 0.140 | |

| R2 Adj. | 0.259 | 0.126 | |

| AIC | 7656.2 | 12117.1 | 6863.2 |

| BIC | 7697.8 | 12158.7 | 6899.7 |

| Log.Lik. | -6049.534 | -3422.581 | |

| F | 38.495 | 9.792 | |

| RMSE | 953.68 | 746.18 | 718.92 |

8.2.1 Truncated normal distribution

Question: How can these models be interpreted?

Needed: Better understanding of truncated (normal) distributions.

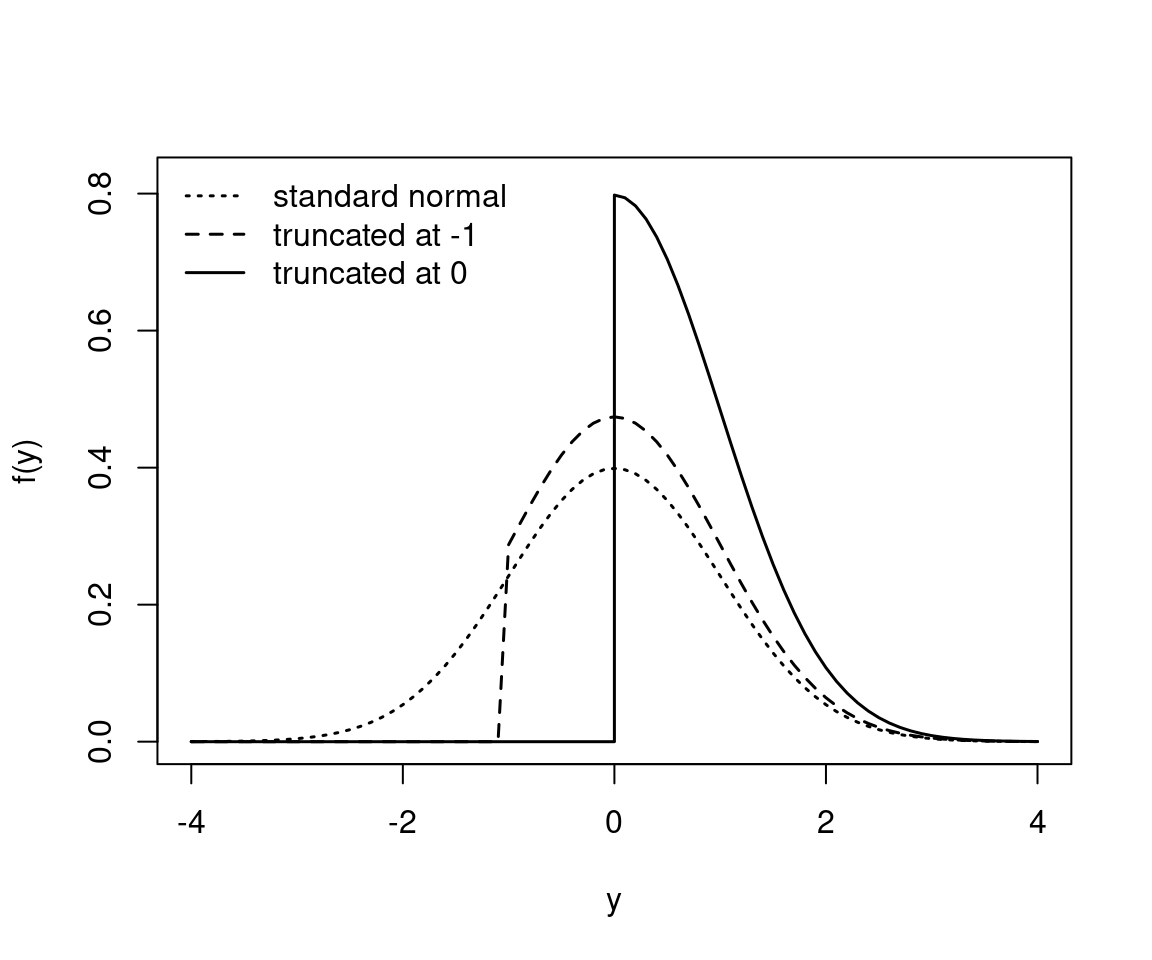

Probability density function: Random variable \(y\) with density function \(f(y)\), truncated from below at \(c\). General form and \(\mathcal{N}(\mu, \sigma^2)\) distribution.

\[\begin{eqnarray*} f(y ~|~ y > c) & = & \frac{f(y)}{\text{P}(y > c)} ~=~ \frac{f(y)}{1 - F(c)} \\ & = & \frac{1}{\sigma} \cdot \phi\left( \frac{y - \mu}{\sigma} \right) \left/ \left\{ 1 - \Phi \left(\frac{c - \mu}{\sigma} \right) \right\} \right. \end{eqnarray*}\]

Example: Standard normal distribution truncated at \(c = -1\) and \(c = 0\).

Figure 8.4: Standard normal distribution truncated at two different points

Expectation: For \(\varepsilon \sim \mathcal{N}(0, 1)\).

\[\begin{eqnarray*} \text{E}(\varepsilon ~|~ \varepsilon > c) & = & \int_c^\infty \varepsilon \cdot f(\varepsilon ~|~ \varepsilon > c) ~d \varepsilon \\ & = & \frac{1}{1 - \Phi(c)} ~ \int_c^\infty \varepsilon \cdot \phi(\varepsilon) ~d \varepsilon \\ & = & \frac{1}{1 - \Phi(c)} ~ \left\{ \left. - \phi(\varepsilon) \phantom{\frac{.}{.}} \! \right|_c^\infty \right\} \\ & = & \frac{\phi(c)}{1 - \Phi(c)} \end{eqnarray*}\]

Because \(\phi'(x) = -x \cdot \phi(x)\).

Note: This simple solution does not hold in general.

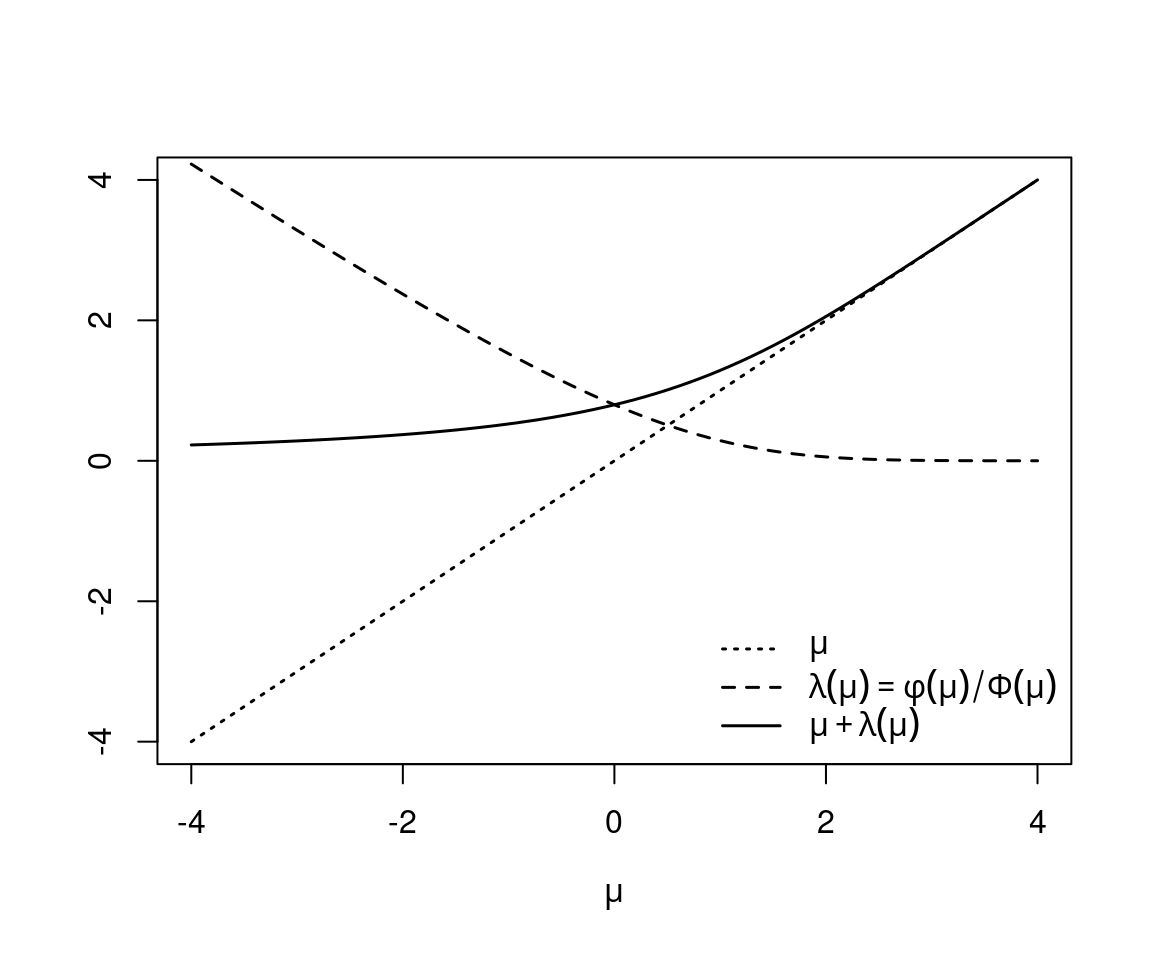

Inverse Mills ratio: Defined as

\[\begin{equation*} \lambda(x) ~=~ \frac{\phi(x)}{\Phi(x)}. \end{equation*}\]

Hence, due to symmetry of the normal distribution, the following holds for \(\varepsilon \sim \mathcal{N}(0, 1)\) and \(y \sim \mathcal{N}(\mu, \sigma^2)\), respectively:

\[\begin{eqnarray*} \text{E}(\varepsilon ~|~ \varepsilon > c) & = & \lambda(-c), \\ \text{E}(y ~|~ y > c) & = & \mu ~+~ \sigma \cdot \lambda\left(\frac{\mu - c}{\sigma}\right). \end{eqnarray*}\]

Example: \(y \sim \mathcal{N}(\mu, 1)\) with truncation at \(c = 0\).

Figure 8.5: Mean and Inverse Mills ratio

8.2.2 Interpretation of the tobit model

Uninteresting: Expectation of latent variable is straightforward but lacks substantive interpretation.

\[\begin{equation*} \text{E}(y^* ~|~ x) ~=~ x^\top \beta \end{equation*}\]

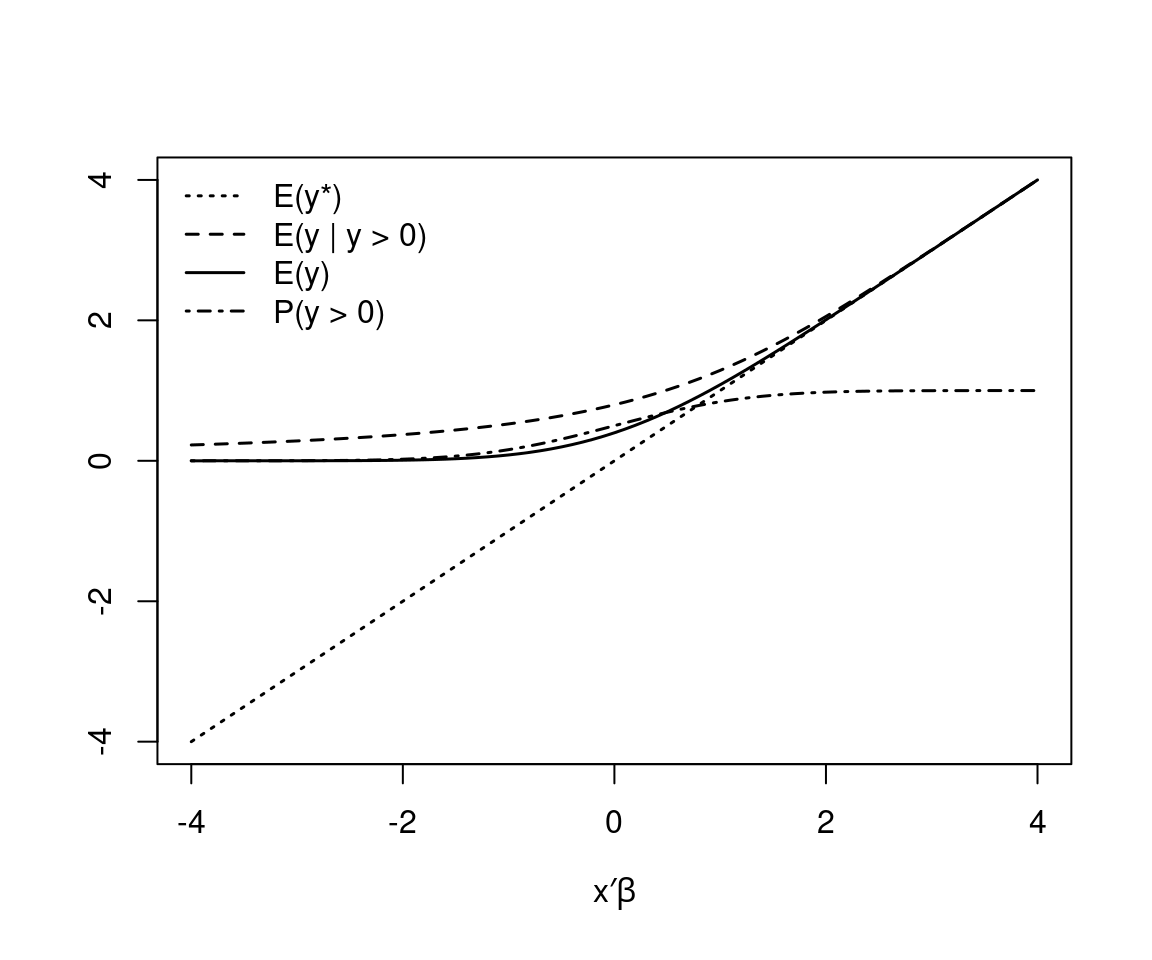

Of interest: Depending on substantive question, consider

\[\begin{eqnarray*} \text{P}(y > 0 ~|~ x) & = & \Phi(x^\top \beta / \sigma),\\ \text{E}(y ~|~ y > 0,~ x) & = & x^\top \beta ~+~ \sigma \cdot \lambda(x^\top \beta / \sigma),\\ \text{E}(y ~|~ x) & = & \text{P}(y > 0) \cdot \text{E}(y ~|~ y > 0,~ x) \\ & = & \Phi(x^\top \beta / \sigma) \cdot \left\{ x^\top \beta ~+~ \sigma \cdot \lambda(x^\top \beta / \sigma) \right\}. \end{eqnarray*}\]

Example: For \(\sigma = 1\).

Figure 8.6: Expectation of the latent and the observed truncated variable

Marginal effects:

\[\begin{eqnarray*} \frac{\partial \text{P}(y > 0 ~|~ x)}{\partial x_l} & = & \phi(x^\top \beta / \sigma) \cdot \beta_l / \sigma\\[0.5cm] \frac{\partial \text{E}(y ~|~ y > 0,~ x)}{\partial x_l} & = & \beta_l \cdot \left[ 1 - \lambda(x^\top \beta / \sigma) ~ \{ x^\top \beta / \sigma ~+~ \lambda(x^\top \beta / \sigma) \}\right] \\[0.5cm] \frac{\partial \text{E}(y ~|~ x)}{\partial x_l} & = & \frac{\partial \text{P}(y > 0 ~|~ x)}{\partial x_l} \cdot \text{E}(y ~|~ y > 0,~ x) ~+~ \\ & & \text{P}(y > 0 ~|~ x) \cdot \frac{\partial \text{E}(y ~|~ y > 0,~ x)}{\partial x_l} \\ & = & \beta_l \cdot \Phi(x^\top \beta / \sigma) \\ \end{eqnarray*}\]

Remarks:

- Overall effect on \(\text{E}(y ~|~ x)\) is sum of an effect at the

- extensive margin (e.g., how much more likely a person is to join the labor force as education increases times the expected hours) and an effect at the

- intensive margin (e.g., how much the expected hours of work increase for workers as education increases times the probability of participation).

- OLS estimation (both for full and positive sample) is biased towards zero due to inability to capture non-constant marginal effects.

- Effects (e.g., at mean regressors) can again be considered instead of marginal effects.

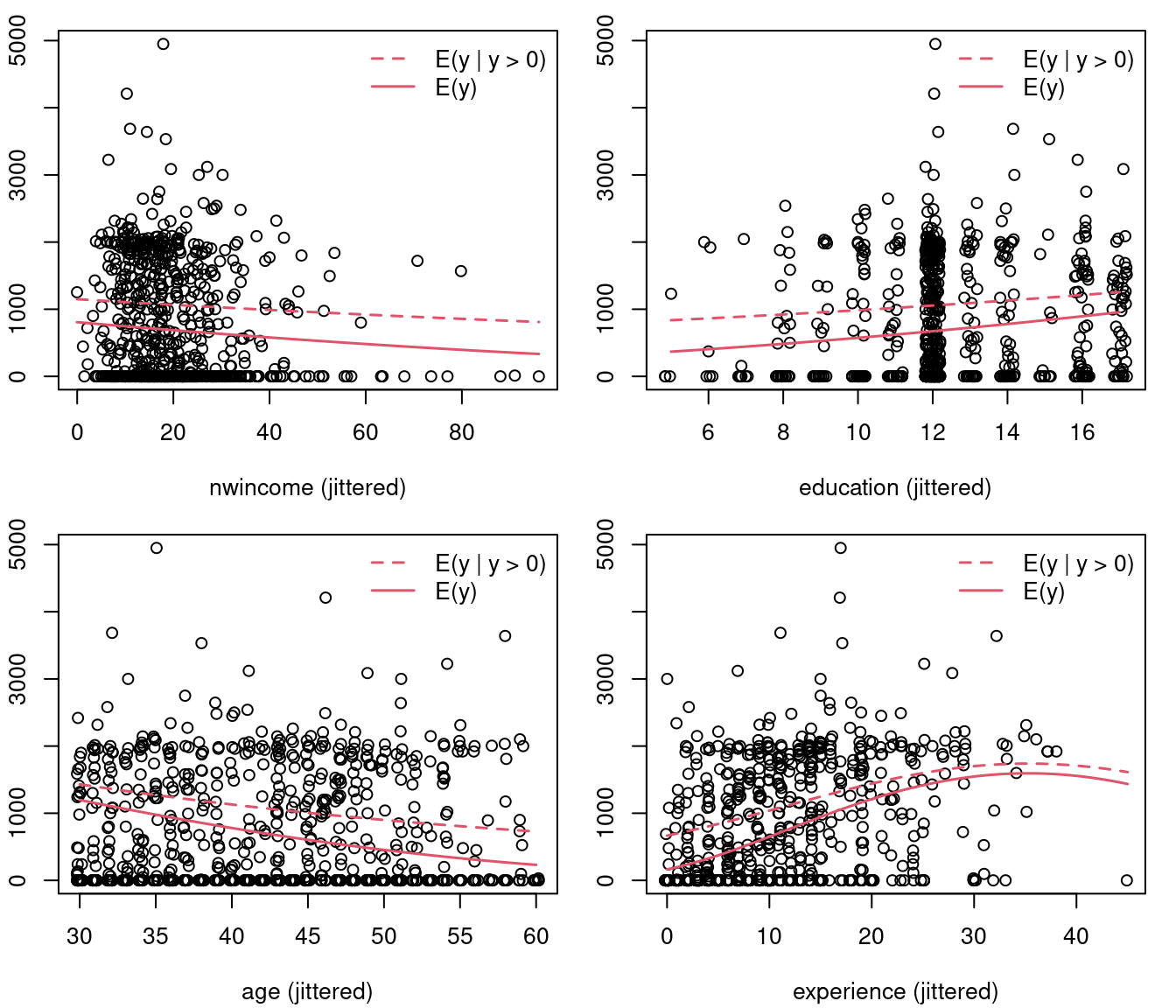

Example: Effects in tobit model for PSID 1976 data (hand-crafted).

Figure 8.7: Effects in tobit model for PSID 1976 data (hand-crafted)

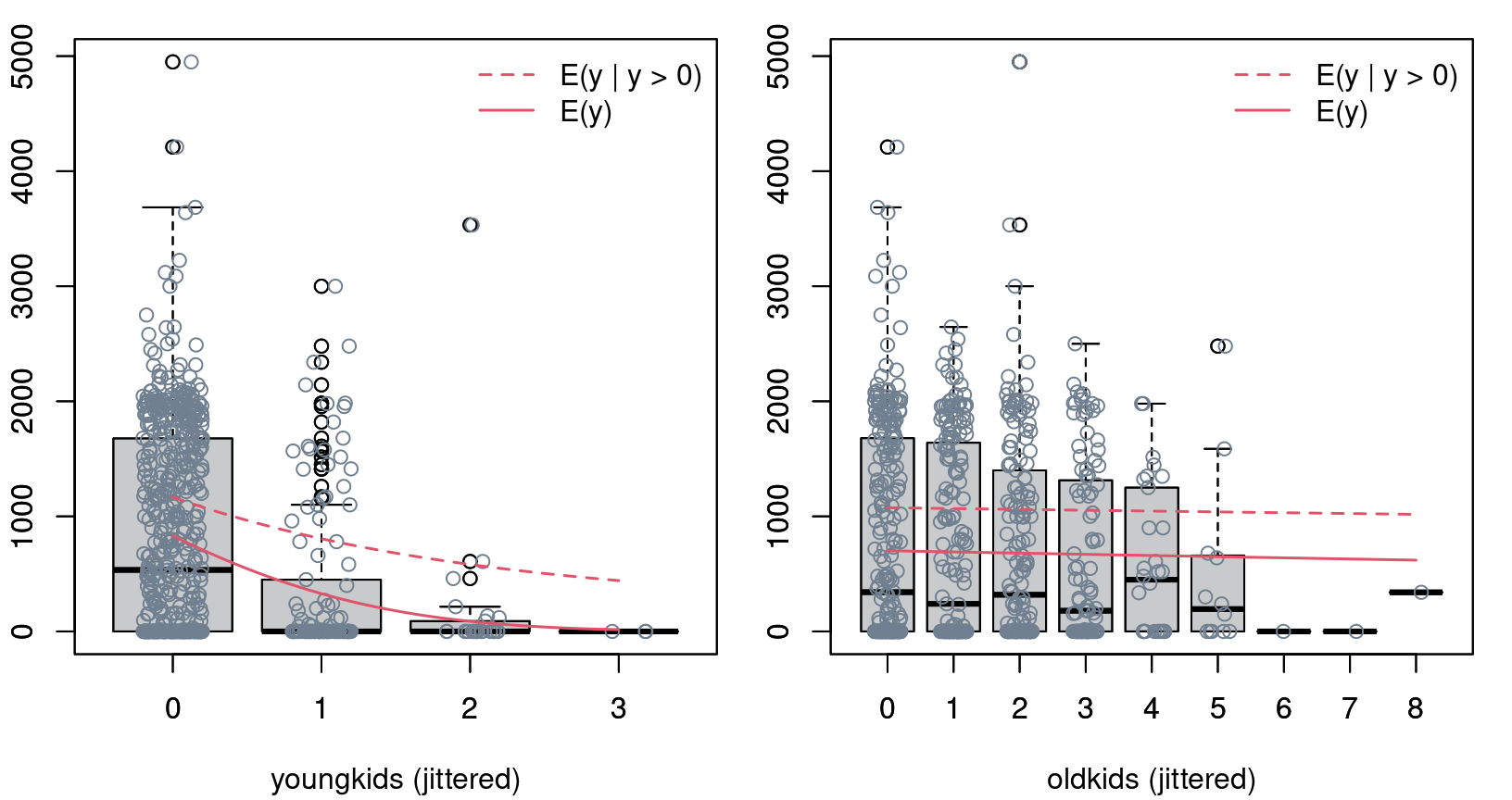

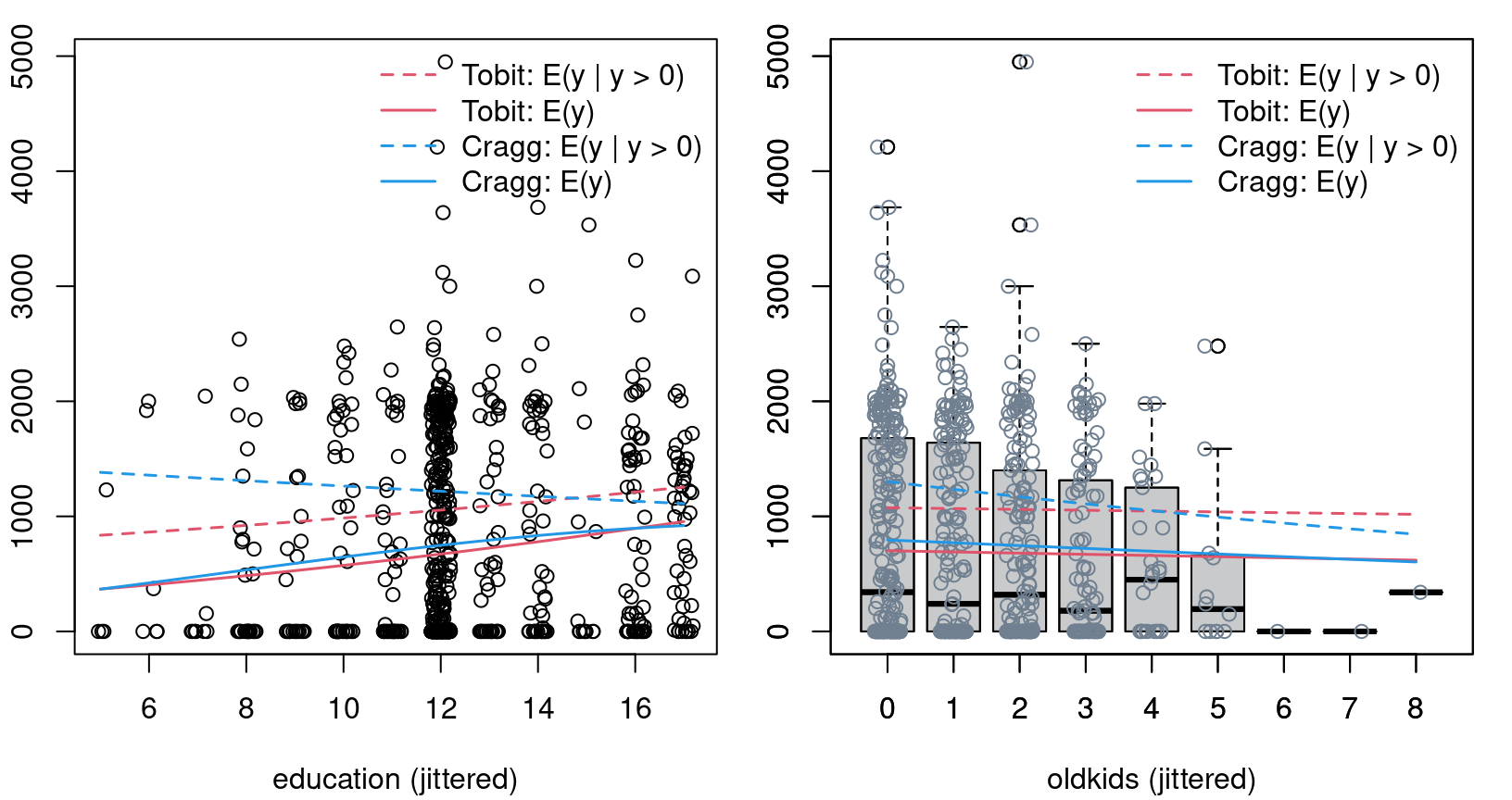

Figure 8.8: Effects of young- and old kids in tobit model for PSID 1976 data

Specification issues:

- The classical (uncensored) OLS regression model is rather robust to misspecifications of distributional form and even non-constant variances. Estimates remain consistent.

- In the tobit model, this is not the case. Misspecification of the likelihood (including constant variances) will lead to misspecification of the score. Hence, \(\text{E}(y ~ |~ y > 0,~ x)\) and \(\text{E}(y ~|~ x)\) are misspecified and estimates inconsistent.

- Crucial assumption: The same latent process drives the probability of a corner solution and the expectation of positive outcomes.

- Example: A single factor, such as number of old kids, can not increase the probability to work but decrease the expected number of hours conditional on participation in the labor force.

- Check for the latter: Cragg two-part model.

8.3 Cragg Two-Part Model

Idea: Similar to hurdle model for count data, employ two parts.

- Is \(y\) equal to zero or positive?

- If \(y > 0\), how large is \(y\)?

Formally: Likelihood has two separate parts.

- \(\text{P}(y > 0 ~|~ x)\): Binomial model (typically probit) for \(I(y > 0)\).

- \(\text{E}(y ~|~ y > 0,~ x)\): Truncated normal model for \(y\) given \(y > 0\).

Remarks:

- The tobit model is nested in the two-part model with probit link. Thus, LR tests etc. can be easily performed.

- If the tobit model is correctly specified, estimates from the probit model \(\hat \gamma\) would be consistent (but less efficient) for the scaled coefficients from the tobit model. Thus, \(\hat \beta / \hat \sigma\) should be similar to \(\hat \gamma\) in empirical samples.

In R: Employ separate modeling function. glm() with "probit" link can be used for selection part.

part_f <- update(hours_f, participation ~ .)

part_probit <- glm(part_f, data = PSID1976,

family = binomial(link = "probit"))

coeftest(part_probit)##

## z test of coefficients:

##

## Estimate Std. Error z value Pr(>|z|)

## (Intercept) 0.27007 0.50808 0.53 0.5950

## nwincome -0.01202 0.00494 -2.43 0.0149

## education 0.13090 0.02540 5.15 2.6e-07

## experience 0.12335 0.01876 6.58 4.8e-11

## I(experience^2) -0.00189 0.00060 -3.15 0.0017

## age -0.05285 0.00846 -6.25 4.2e-10

## youngkids -0.86833 0.11838 -7.34 2.2e-13

## oldkids 0.03601 0.04403 0.82 0.4135truncreg() from package truncreg (or trch() from package crch) can be employed for estimating the truncated normal regression model.

library("truncreg")

hours_trunc <- truncreg(hours_f, data = PSID1976,

subset = participation == "yes")

coeftest(hours_trunc)##

## z test of coefficients:

##

## Estimate Std. Error z value Pr(>|z|)

## (Intercept) 2055.713 461.265 4.46 8.3e-06

## nwincome -0.501 4.935 -0.10 0.91912

## education -31.270 21.796 -1.43 0.15139

## experience 73.007 20.229 3.61 0.00031

## I(experience^2) -0.970 0.581 -1.67 0.09521

## age -25.336 7.885 -3.21 0.00131

## youngkids -318.852 138.073 -2.31 0.02093

## oldkids -91.620 41.202 -2.22 0.02617

## sigma 822.479 39.320 20.92 < 2e-16Comparison of (scaled) parameter estimates from tobit, probit, and truncated model.

cbind("Censored" = coef(hours_tobit) / hours_tobit$scale,

"Threshold" = coef(part_probit),

"Truncated" = coef(hours_trunc)[1:8] / coef(hours_trunc)[9])## Censored Threshold Truncated

## (Intercept) 0.860327 0.270074 2.4994098

## nwincome -0.007856 -0.012024 -0.0006093

## education 0.071875 0.130904 -0.0380188

## experience 0.117256 0.123347 0.0887641

## I(experience^2) -0.001661 -0.001887 -0.0011788

## age -0.048488 -0.052852 -0.0308044

## youngkids -0.796795 -0.868325 -0.3876719

## oldkids -0.014454 0.036006 -0.1113943LR test and information criteria:

loglik <- c("Tobit" = logLik(hours_tobit),

"Two-Part" = logLik(hours_trunc) + logLik(part_probit))

df <- c(9, 9 + 8)

-2 * loglik + 2 * df## Tobit Two-Part

## 7656 7620## Tobit Two-Part

## 7698 7698## Two-Part

## 1.273e-08

Figure 8.9: Education and oldkids effects in Tobit and Cragg model

8.4 Sample Selection Models

Idea: Employ censored regression model for observations \(y ~|~ y > c\) but model censoring threshold \(c\) as random variable.

Name: Incidental censoring or self selection.

Example: Distribution of wages.

- Wages are only observed for workers.

- Thus, the wages that non-workers would receive (if they decided to work) are unknown/latent.

- Individuals decide to work if their (possibly latent) offered wage \(w_0\) exceeds their individual reservation wage \(w_r\).

- The distribution of wages for workers are thus \(f(w_o ~|~ w_o > w_r)\) with random \(w_r\).

Formally: With \(y\) and \(c\) stochastic rewrite

\[\begin{equation*} f(y ~|~ y > c) ~=~ f(y ~|~ y - c > 0) ~=~ f(y_1 ~|~ y_2 > 0). \end{equation*}\]

Special cases:

- \(y_1 = y_2\): Standard censoring regression (i.e., tobit).

- \(y_1\) and \(y_2\) independent: \(f(y_1 ~|~ y_2 > 0) = f(y_1)\) (i.e., no selection).

Simple approach: Bivariate normal distribution for \((y_1, y_2)\) with correlation \(\varrho\), including special cases \(|\varrho| = 1\) (identity) and \(\varrho = 0\) (independence).

Alternatively: Employ different bivariate distribution or semiparametric approach.

Regression model: Employ (potentially overlapping) regressors for mean of both components.

\[\begin{eqnarray*} \mbox{Outcome equation:} & y_1 ~= & x^\top \beta ~+~ \varepsilon_1, \\ \mbox{Selection equation:} & y_2 ~= & z^\top \gamma ~+~ \varepsilon_2, \end{eqnarray*}\]

where

\[\begin{equation*} \left( \begin{array}{cc} \varepsilon_1 \\ \varepsilon_2 \end{array} \right) ~\sim~ \mathcal{N}\left( \left( \begin{array}{cc} 0 \\ 0 \end{array} \right), \left( \begin{array}{cc} \sigma^2 & \varrho \\ \varrho & 1 \end{array} \right) \right). \end{equation*}\]

Remarks:

- Observation rule: \(y_1\) is non-censored, observed for \(y_2 > 0\).

- In selection equation, only \(y_2 > 0\) vs. \(y_2 \le 0\) is observed. Hence, standardize \(\text{Var}(y_2) = 1\) for identifiability (as in probit model).

- Terminology: Heckman model, heckit model, sample selection model, self-selection model, tobit-2 model.

Conditional expectation:

\[\begin{equation*} \text{E}(y_1 ~|~ y_2 > 0,~ x) ~=~ x^\top \beta ~+~ \sigma \cdot \varrho \cdot \lambda(z^\top \gamma). \end{equation*}\]

Selection effect: Sample is

- positively selected for \(\varrho > 0\): \(\text{E}(y_1 ~|~ y_2 > 0,~ x) > \text{E}(y_1 ~|~ x)\),

- negatively selected for \(\varrho < 0\),

- and no selection occurs for \(\varrho = 0\).

Estimation:

- Efficient: Full maximum likelihood.

- Biased: OLS for non-censored observations.

- Consistent (and employed only for historical reasons): Two-step estimator. Probit model yielding \(\hat \gamma\) followed by OLS regressing \(y\) on \(x\) and \(\lambda(z^\top \hat \gamma)\).

Classical example: Estimation of mean wage offers (or worker’s productivity) from a sample of workers and wages.

In this context: Sample selection model called Gronau-Heckman-Roy model (by Winkelmann & Boes 2009) due to the authors that first recognized this problem and established its inference, respectively.

Identification: Economic considerations guide selection of variables \(x\) that affect the outcome and variables \(z\) that affect the selection.

- Typically, all variables \(x\) for the outcome also affect selection, especially in the case of “self selection”.

- Additional variables might affect the selection but not the outcome. Example: Presence of small children will affect selection but probably not the reservation wage.

- Such variables play a similar role as “instruments”.

Example: Female wages in PSID 1976 data. Employ semi-logarithmic wage equation with education and quadratic polynomial in experience.

OLS estimation: For selected subsample.

Sample selection model: Additionally employ age, number of old and young children, and other income as regressors in selection equation (corresponding to previously used part_f).

In R available in selection() from package sampleSelection:

Sample selection models

##

## z test of coefficients:

##

## Estimate Std. Error z value Pr(>|z|)

## (Intercept) 0.266449 0.508958 0.52 0.6006

## nwincome -0.012132 0.004877 -2.49 0.0129

## education 0.131341 0.025382 5.17 2.3e-07

## experience 0.123282 0.018724 6.58 4.6e-11

## I(experience^2) -0.001886 0.000600 -3.14 0.0017

## age -0.052829 0.008479 -6.23 4.7e-10

## youngkids -0.867399 0.118651 -7.31 2.7e-13

## oldkids 0.035872 0.043475 0.83 0.4093

## (Intercept) -0.552696 0.260379 -2.12 0.0338

## education 0.108350 0.014861 7.29 3.1e-13

## experience 0.042837 0.014879 2.88 0.0040

## I(experience^2) -0.000837 0.000417 -2.01 0.0449

## sigma 0.663398 0.022707 29.21 < 2e-16

## rho 0.026607 0.147078 0.18 0.8564Interpretation: \(\hat \varrho\) is essentially zero signaling that there are no significant selection effects. Outcome part of Gronau-Heckman-Roy model and OLS for selected subsample are thus virtually identical.

## GHR (outcome) OLS (positive)

## (Intercept) -0.5526963 -0.5220406

## education 0.1083502 0.1074896

## experience 0.0428368 0.0415665

## I(experience^2) -0.0008374 -0.0008112Similarly: Selection part of Gronau-Heckman-Roy model and probit for selection are thus virtually identical.

## GHR (selection) Probit (0 vs. positive)

## (Intercept) 0.266449 0.270074

## nwincome -0.012132 -0.012024

## education 0.131341 0.130904

## experience 0.123282 0.123347

## I(experience^2) -0.001886 -0.001887

## age -0.052829 -0.052852

## youngkids -0.867399 -0.868325

## oldkids 0.035872 0.036006Effects: Compare education effects graphically.

Set up auxiliary data with average regressor and varying education.

X <- model.matrix(hours_tobit)[, -c(1, 5)]

psid <- lapply(colnames(X), function(i)

if(i != "education") mean(X[,i]) else

seq(from = min(X[,i]), to = max(X[,i]), length = 100))

names(psid) <- colnames(X)

psid <- do.call("data.frame", psid)Predictions for OLS:

Compute predictions for sample selection model by hand:

xb <- model.matrix(delete.response(terms(wage_f)),

data = psid) %*% coef(wage_ghr, part = "outcome")

zg <- model.matrix(delete.response(terms(part_f)), data = psid) %*%

head(coef(wage_ghr), 8)

wage_ghr_out <- xb + coef(wage_ghr)["sigma"] *

coef(wage_ghr)["rho"] * dnorm(zg)/pnorm(zg)

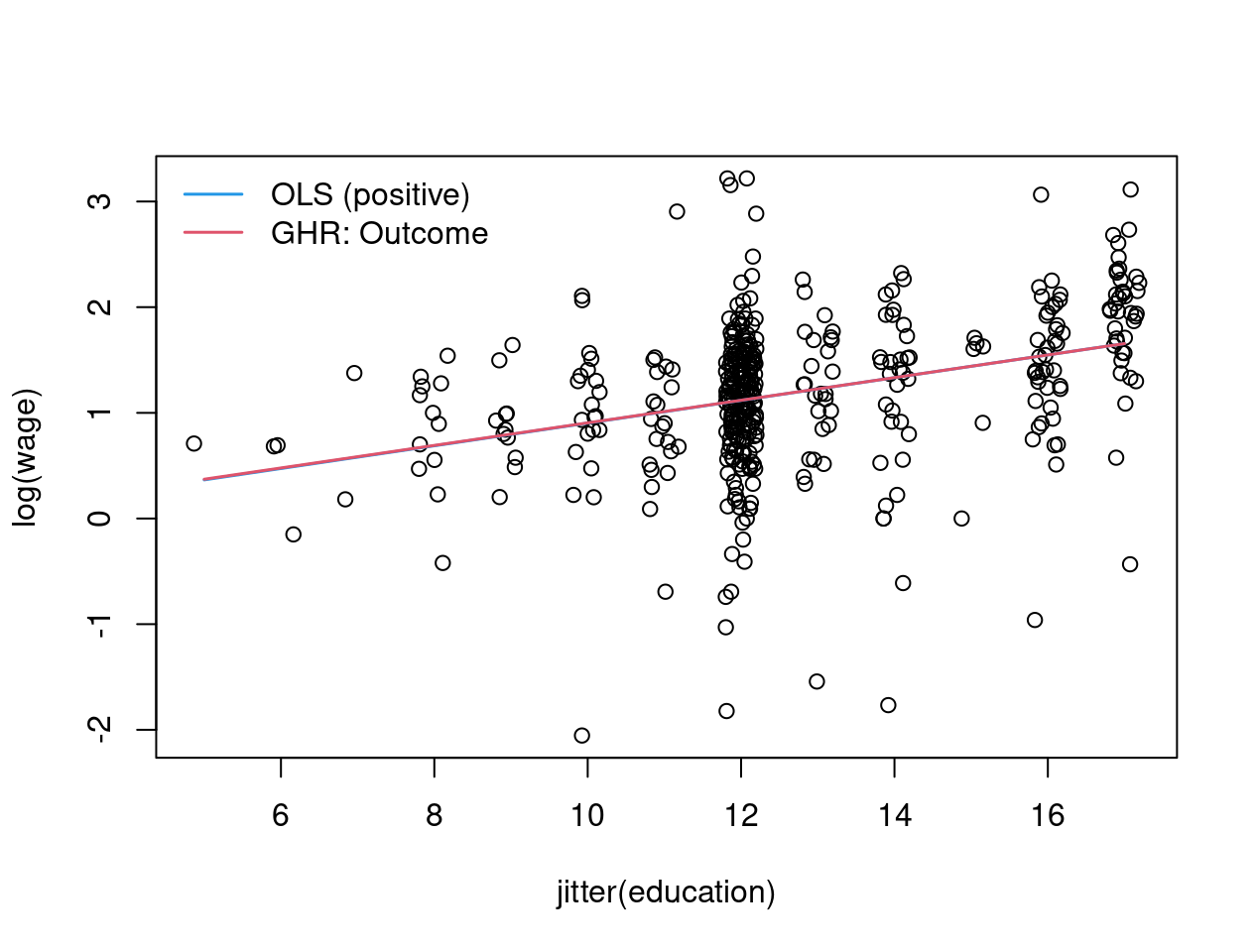

Figure 8.10: Sample selection model: education against log(wage) - jittered